DEMOCRATIC REPUBLIC OF CONGO (DRC)

Katanga Mining Ltd (KML)

Kamoto Mining project

See outline of the project

See outline of the project

See outline of the project

See outline of the project

The sponsors of this project are under criticism in Congo, Belgium, the UK, Canada and South Africa, because it is thought to be unfair to local communities and to favorable to the foreign party. See critics in the left frame, particularly these two because they explain well the opposition: one is from a Congolese source; and this one is from Mining Watch Canada.

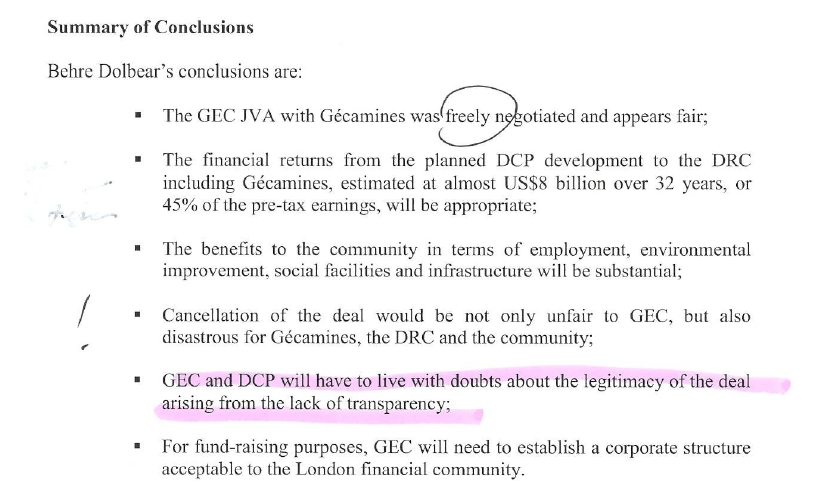

Those in favour of the project argue that the mining convention has been reached in accordance with the mining law of 2002, that Gécamines's interests have been preserved, that the projet will give employement to 12 000 and their families and sustain activity for 240 000 people over project llifetime of 20 years. See these arguments in the praise links of the left frame. Of which this one which denounces international NGO's including RAID UK. And this one "GAForrest's address on the day of official transfer of Gécamines's facilities to Kamoto Copper Company".A justification of similar Joint Venture Agreements between Gécamines and foreign mining companies created for the purpose of taking over mining assets is made in Behre Dolbear's letter to GEC for the project KOV.  See the conclusion of this letter.

See the conclusion of this letter.

In accordance with the JV agreement signed with Gécamines (Gécamines), KML have undertaken a feasibility study of the project. A "Technical Report" with an economic analysis has been produced which shows sources and uses of funds over the 20 year life of the project. A definitive feasibility report for implementation of the project is presently underway.

Information Disclaimer

The information provided in this web site is only intended to be general public information. The content viewed on this site, including news, documents, quotes, data and other information, is provided by me, Pierre Ratcliffe retired mining engineer with residence at Callian 833440 France, from compilations of material published on the Internet. Content on this site is not appropriate for the purposes of making a decision to carry out a transaction or trade. Nor does it provide any form of advice (investment, tax, legal) amounting to investment advice, or make any recommendations regarding particular financial instruments, investments or products or mining agreement. The processing of all data accessed on the Internet, notably data published by KML on their website, is used to undertake an independant economic assessement, with a view to understanding the sharing of profits (net surplus cash generated over the 20 year project lifetime). The methodology used is myown and the results of the assessement, presented in a neutral form, are matter of opinion over future development. Thus they cannot be claimed as being harmful to the reputation of KML or KCC.

I do not question the "Technical Report" which has been performed by a multi-disciplinary team of reputed mining and metallurgical experts independently of KML. Their work appears to have been done according to the state of the art, in particular, for geological reserve estimates - in the categories of certainty: measured, proven, inferred, and probable - cut off grades have been established to quantify economically recoverable reserves, underground mining plans are made according to professional standards, openpit distribution of grades have been established using geostatistical methods, ultimate pit configurations have been drawn based on the computed cut-off grades and 3 dimensional block modelling... This work is professional without doubt. Of course there are always elements that can be questioned and that are subject to debate between geologists, mining and metallurgical specialists. But such questioning is out of the scope of this essay. I shall therefore use the data of this Technical Report.

I concentrate on the economic aspects of the project in order to elaborate the means to assess if the interests of Gécamines and of the local communities as well as of Katanga and DRC are taken care of in fairness.

With the capital and operating cost estimates given in the Technical Report, and copper/cobalt prices cif ex Durban RSA to Europe/US/China/Corea/Japan of 1.1/10 US$/lb, the internal rate of return of the project, the IRR, is 29.3%. This IRR is high, if it is referred to the opportunity cost of capital in developed countries of circa 4% in constant money value (6% in current) because it leaves a margin of 25.3%. But in DRC the opportunity cost of capital carries a risk factor for investors. This is considered here as 8% in constant money value. So the opportunity cost of capital in RDC is taken as 12% and this will be used as a base case to discount monetary flows of the project. As will be seen in the assessement model, the discounting factor can be changed at will.

The opportunity cost of capital defined above corresponds to the discounting factor used to calculate present worth values of monetary flows. The discounting factor eg. 12% is the rate of interest that is applied to a revenue expected in the future, for example year-end 12, to calculate the value of that revenue in year one (PV) ie. the amount to be deposited in a bank at 12% compounded interest that will yield 100 M$ at the end of year 12. If 100M$ is expected at year-end 12, its discounted value or present value PV 12% is 100/(1+0.12)12 ie. 25.67M$. With a 6% value for the discounting factor, the PV 6% of 100M$ at year-end 12 is 50.66M$. The present worth value of a flow of revenues spread over 20 years at a discounting factor of 12%, noted PWV@12%, is the sum of PVs 12% of each annual revenue. The internal rate of return IRR is the value of the discounting factor, that renders PWV nil; this can be noted PWV@irr%=0.

Then the base case IRR for the project sponsors, with the data considered, is 17.3% above the opportunity cost of capital of 12%. If it is effectively the case, the project will produce revenues for developing other mines, or investing in other industrial projects in RDC and/or in other parts of the world. This rate of return is shared between the project owners, ie. KML and Gécamines at 75% and 25% respectively, within a Joint Venture Company ie. KCC (Kamoto Copper Company). KCC was created in order that Gécamines could transfer its properties to a private company that could enter into an agreement with a foreign partner. This is the outcome of a privatization process of state enterprises by the DRC, under pressure by international financing institutions and the implementation of structural adjustment programmes in order to restore the country's debt worthiness.See details on this by RELCOF (Réseau de lutte contre la corruption et la fraude) : "Bradage Criminel du Patrimoine Minier du Congo". And also this link which explains the historical background and the geopolitical stakes of the international mining companies in the Democratic Republic of Congo (dated december 1999).

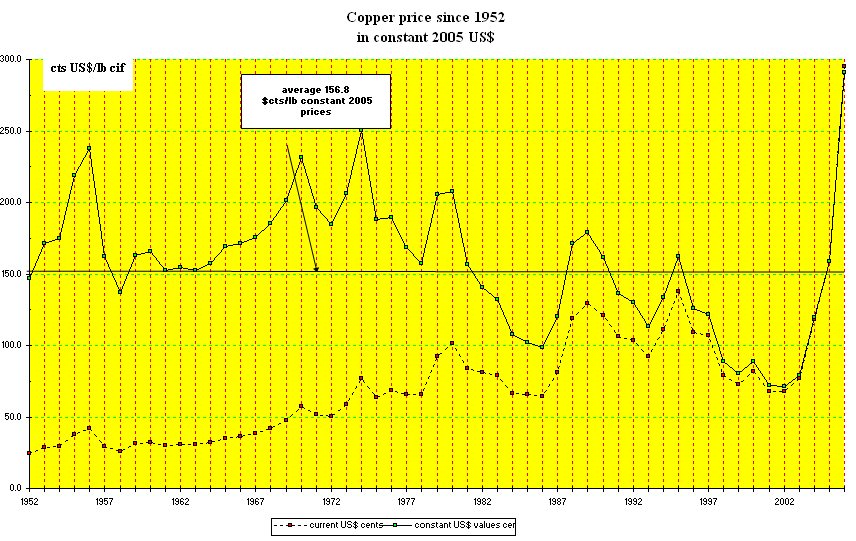

Cu and Co prices 1900-2004 in current US$/lb and 2004 US$/lb using consumer price index series. Average prices 1952-2004 and 1984-2004 have benne computed (see Cu and Co tabs in each table).With Cu/Co price increases in 2005, the 53 year (1952-2005) average price of copper, in constant 2005 US$/lb, is 1.57$/lb.  See historic trend which does show a regular increase of copper price in constant $ value, even disregarding the very sharp price increases in 2005-2006. Recently there has been a dramatic increase of copper prices due to growth of demand in fast developing China and India and inadequate supply.

See historic trend which does show a regular increase of copper price in constant $ value, even disregarding the very sharp price increases in 2005-2006. Recently there has been a dramatic increase of copper prices due to growth of demand in fast developing China and India and inadequate supply.  See prices 11/1998-11/2006 in current US$/mt values. In 2006 average transactions at LME were above 2.5$/lb Cu.

See prices 11/1998-11/2006 in current US$/mt values. In 2006 average transactions at LME were above 2.5$/lb Cu.

In consideration of this evolution, KML have increased the Cu price considered in their reports to the market to 1.25US$/lb.

The historical price of Co over the same period is 15US$/lb 100% Co content.  See historical price Co 1952-2004.

See historical price Co 1952-2004.

The copper and cobalt prices of 1.10 US$/lb and 10.0 US$/lb considered in KML's "Technical Report" are therefore conservative as the average Cu price 1952-2005 in 2005 US$ is 1.57 US$/lb and the average Co price is 15$/lb. The project lifetime is 20 years, so the average price over this period may be higher or lower than the average price over 53 years. However, the long term trend is an increase of prices and the recent sharp increase due to consumption in China and India, and also inadequate supply, suggest that the trend for price increase will confirm. So, my opinion, is that average Cu and Co price over the 20 year project lifetime will be higher than the 53 year average price, 1952-2005 of 1.57/15US$/lb 2005 value.

early stages of negotiation. Presumably, it was not adopted because the economics of the project - ie. the Cu/Co prices of 1.1/10 US$/lb - would have favoured Gécamines to much and KML to little. And it should be mentioned the Gécamines receives a royalty of 2-1.5% on project sales values ex-plants (2% in the first 3 years, 1.5% afterwards).

To assess fairness of the JVA to Gécamines, one has to estimate the respective shares of KML, Gécamines and DRC state in the surplus cash generated by the project. This can be done by determining the discounted value of these shares in US$ values, ie. present worth values at the discounting factor (PWVs at DF). As mentioned earlier the discounting factor is taken as 12% which includes 8% risk factor for DRC. The exercise is done in constant value of money, ie. with no inflation of prices and costs which would complicate the model to much. However, the effect of this may be examined by sensitivity to price variations, as well as operating costs.

Gécamines's share should be related, in some manner ie. with a percentage of discount, to the real value of assets transferred by Gécamines to the JV company KCC ie. geological reserves measured and proven which are of a high degree of certainty, and the age and quality of existing plant and equipment, as this value affects the additional capital required for resuming production; and this capital is entirely provided by the foreign party KML. See existing assets. Therefore, Gécamines PWV at 12% DF should be referred to the value of assets transferred. The value of the assets transferred is reflected in KML's project overview. This overview states that underground mining can resume quickly and at low cost, that the Kamoto concentrator and the metallurgical plants of Luilu are in good condition and therefore could also treat third party ore. And the main asset transferred is the Cu/Co reserve of the category proven and probable.  See summary reserve tablulation which shows a total reserve of circa 3 million tonnes Cu/Co in Cu equivalent at prices 1.5/15 $/lb. It is significant to note that the Cu/Co production during the life of the project will deplete only % of Cu proven and probable reserves and % of Co proven and probable reserves.

See summary reserve tablulation which shows a total reserve of circa 3 million tonnes Cu/Co in Cu equivalent at prices 1.5/15 $/lb. It is significant to note that the Cu/Co production during the life of the project will deplete only % of Cu proven and probable reserves and % of Co proven and probable reserves.

The model must enable to assess the effect of Cu/Co price variations, the effect of introducing a downpayment of front money and the effct of a change in % share of Gécamines in KCC, on the sharing of project net surplus cash, between KML, Gécamines and DRC.

The approach I use is the following. On the basis of the data of KML's "Technical Report" and of the cost estimates therein, I have developed an Excel spreadsheet to calculate the internal rate of return of the project ie. the rate of interest that makes nil the 20 year schedule of gross cashflow:

gross cashflow = sales - capital investments - direct operating costs.

NB: direct operating costs include royalty payments to DRC and to Gécamines calculated as 2% of sales value ex plants.

See a course on economic evaluations of mining projects, of which this  diagram on the flow of cash.

diagram on the flow of cash.

Note: I have made an adjustment to the so called "DRC benefits" of the "Technical Report". The report lists direct costs and indirect costs ie. royalties, taxes on income and dividend tax. The two latter costs have been discarded in my assessement of the IRR.  See these data.

See these data.

The model (an Excel spreadheet) can be downloaded by clicking on this link. Once downloaded, one can use the model and play around with the figures. A sheet "how to use" is included.

Having developed this model, I have built a sensitivity sheet in the Excel spreadheet, which I call "sharing". In this sheet, I calculated the IRR of the project, and from thereonwards, I tabulated the sources and uses of funds in order to derive an estimate of net surplus cash generated by the project. I have assumed that KML would finance capital costs 50% by equity and 50% by loans at 12% interest - ie. the opportunity cost of capital - over 10 years. From there I have calculated the PWVs at 12% of KML, Gécamines, DRC and loaners respectively; adding these PWVs and comparing them to the total PWV of the project, I have balanced the two by creating a front money payment to Gécamines. This Excel spreadsheet is fully versatile; all the parameters can be changed and their effect on respective shares can be displayed immediately.

NB: the PWV at 12% of the loaners is nil (disbursements and repayments of capital and interest), because their rate of interest is also 12%.

The results of changing Cu/Co prices and % sharing of profits, are given in the sheets  "share25%" and

"share25%" and  "share49%".

"share49%".

As a result of these calculations, it can be seen that the "Technical Report" base case ie. Cu/Co prices 1.1/10$/lb, Gécamines 25% sharing and no downpayment, corresponds to respective shares of the project's PWVs at 12% of KML 27.1%, Gécamines 26.7%, DRC 46.3%, loaners 0%. And the total PWV at 12% for Gécamines comes to 143.2 M$, a value which I believe is far below the real value of assets transferred. So, despite the equivalence in the % sharing of profits KML/Gécamines, this case may be considered as insufficient for Gécamines because the PWV 12% expected for Gécamines may be lower than the real value of assets transferred.

Considering Cu/Co prices 1.52/15$/lb, Gécamines 25% sharing and no downpayment, the same method as above corresponds to respective shares of the project's PWVs at 12% of KML 43.6%, Gécamines 21.4%, DRC 35.1%, loaners 0%. And the total PWV at 12% for Gécamines comes to 351.2 M$.

The latter case may be considered insufficient for Gécamines which reflects in the PWV at 12% differences in % and in total PWV to Gécamines. The way to correct this is to provide for a dowpayment to Gécamines to balance the difference. This amount calculates to 266.3 M$. And the respective shares of the project's PWVs at 12% become KML 38.1%, Gécamines 31.3%, DRC 30.6%, loaners 0%. And the total PWV at 12% for Gécamines comes to 589 M$ which may be closer to the real value of assets transferred.

In view of this, the question is "what is the real value of assets transferred to KML by Gécamines?" according to their book value in the accounts, their physical state and capacity to resume operations, and allowing for a reasonable discount... If this value could be obtained, it would further strengthen the case of what the fair share of total PWV at 12% of the project should be for Gécamines. By comparison Balkashmed copper complex in Kazakstan was estimated at an acquisition price of 450 MUS$ for 180 000mt Cu per year at 0.90 US$/lb. That is 2 500 US$ per tonne year of Cu. For Kamoto, with 115 000t Cu and 6 000t Co, an equivalent 150 000t Cu at 1.1/10$/lb prices, the acquistion price would be of the order of 375 MUS$. The quality of the assets are shown in the november 2006 report of KML on the advancement of the project.

In the base case of the Techical Report, the Cu/Co prices of 1.1/10$/lb are to low to support front money payment for the assets transferred by Gécamines to KCC; the JV agreement's provision for 75/25% sharing of the project's PWV at 12% between KML and Gécamines appear to be correct ie. respectively KML 27.1%, Gécamines 26.7%, while DRC gets 46.3%. This means that the assets have to be transferred at zero value to make the project viable.

With Cu/Co prices of 1.52/15$/lb which are more relevant, the situation is quite different and the JV agreement's provision for 75/25% sharing of the project's PWV at 12% between KML and Gécamines appears to be insufficient for Gécamines ie. respectively KML 43.6%, Gécamines 21.4%, and DRC 35.1%. Cu/Co prices and the project revenues seem to justify in this case, payment of front money to Gécamines. This amount calculates to 266.3 M$. And the respective shares of the project's PWVs at 12% become KML 38.1%, Gécamines 31.3%, DRC 30.6%, loaners 0%. And the total PWV at 12% for Gécamines comes to 589 M$ which may be closer to the real value of assets transferred with a reasonable discount.

In view of the assets transferred by Gécamines to KCC, of their description by KML, of pictures shown on their website, and of my experience of similar projects in Kazakstan, Peru and the Urals, 589 MUS$ seems near the mark; the more so if geological reserves are counted in the degree of certainty measured and proven which reflects costly exploration work done by Gécamines before the transfer.

Because there is no market value for these assets, the only way to obtain the real value of assets transferred by Gécamines to KCC is to visit the site and to run a technical and financial audit of the assets by an independent expert. If the agreement had been reached by a process of international competitive bidding this would not have been a problem.

The agreement between Gecamines and KML has been reached on the basis of non competitive bidding. There is therefore suspicion that the agreement may be flawed in favour of KML for several reasons: eg. undervalued Cu/Co prices which lead to giving KML a number of advantages to compensate, of which transfer of the Gecamines' assets at zero cost and a low participation of Gecamines in future profits.

As it may not be possible to cancel the agreement and go for international competitive bidding, because of the state of advance of implementation of the project, the only way to resolve the issue of suspicion is to renegotiate the contract with a revised combination of front money and participation to future profits.

Further reading:

Updated on 17/01/2015 by Pierre Ratcliffe Contact: (pratclif@gmail.com) web site http://pratclif.com